When considering retirement plans, the many options — not to mention complicated tax rules — leave many employers uncertain about the best plan for their company. One of the basic decisions employers face is whether to offer qualified or non-qualified retirement plans, or some combination of both. Here’s a closer look at the pros and cons of each.

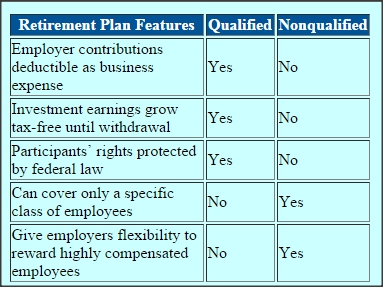

Qualified retirement plans are employer-sponsored retirement plans that “qualify” participants for certain tax benefits by meeting requirements under federal law for coverage,

The major attraction of qualified plans is tax breaks.

Tax Advantages

The major attraction of qualified plans is tax breaks. Employers take a current tax deduction for all plan contributions, while employee accounts grow tax-free until the time of distribution. Some plans do not require the employer to make annual contributions. Employer contributions to qualified plans are held in trust until the employee is entitled to receive them, an arrangement that helps assure employees that the money will actually be there when they retire.

However qualified plans have several drawbacks. Any time an employer makes a contribution, it must make contributions on behalf of all participants. Some plans require employers to make annual contributions whether or not the company is profitable. Benefits are not guaranteed in most plans (although federal law protects participants’ rights), and participants face a substantial penalty for early withdrawals.

In recent years, qualified plans have become less attractive for two reasons: regulatory changes keep whittling down the maximum amount of money that employers can contribute to them and increasingly complex rules are burdening employers with higher administrative costs. This has led to reduced qualified plan benefits for many valuable employees and has limited employers’ ability to adequately compensate these workers. In response, some companies have turned to non-qualified plans to replace the lost benefits.

Non-qualified plans are employer-sponsored plans designed to benefit a select group of executive or key employees. If the plan is properly structured, the employer can include only those employees it chooses — without having to abide by the anti-discrimination, participation or vesting rules that qualified plans must follow.

Although non-qualified plans are subject to fewer government regulations, they receive fewer tax benefits. Any earnings in the plan are taxable to the employer and taxable to the employee when distributed as benefits. However, the employer can take a tax deduction at the time of distribution. And since non-qualified plan contributions are not held in a separate trust, employees receive no guarantee that benefits will be there when they retire — and any assets set aside for future payouts are subject to claims by employers’ creditors.

Irrevocable Trusts

One way to reduce the potential financial risk to non-qualified benefits is by setting up an IRS-approved irrevocable trust into which the employer contributes the plan assets, which are managed and distributed by the trustee. Although these trusts do not protect the assets against creditors’ claims in case of company insolvency, they generally offer protection in the event of a corporate takeover, change in management or other event that could threaten the availability of benefits.

Without a requirement that non-qualified plan assets be held in trust, many companies pay non-qualified benefits out of general corporate assets as they become due. This approach assumes that future growth of the company will cover its benefit obligations. This arrangement might strain the coffers of smaller companies on payout day and leave executives wondering about the security of their benefits.

An alternative to the pay-as-you-go approach is to create an asset reserve for future plan obligations by using corporate-owned life insurance (COLI). Typically, the company buys a cash value life insurance policy — either whole life or universal life — on the life of the key employee and names itself as beneficiary. The employer owns the policy and pays all premiums. After the employee retires, the company can use the policy’s cash value to pay the benefit. If the employee dies, the policy pays a tax-free death benefit to the company.

The advantage of funding with COLI is that the cash accumulation inside the policy grows tax-free. However, COLI offers no protection against any creditor’s claims, so it won’t provide an employee total peace of mind. A trust can hold the COLI; however, trusts have tax implications for both the employer and the participant.

Leave a Reply