Focus on controlling the smaller, more frequent losses —they will impact your ex-mods more than less frequent, larger losses.

Rating bureaus publish rates for hundreds of different job classifications, shown as rate per $100 of payroll. These rates are based on the relative hazards of each occupation. For example, it costs more per $100 of payroll to insure roofers than computer programmers, since roofers are more likely to experience severe on-the-job injuries. To avoid overpaying, you will want to review your company’s occupational categories to make sure your employees haven’t been misclassified.

You can’t change your employees’ job classifications: if an employee performs the duties of a roofer, then your insurer will classify him/her as a roofer. But you do have control over the other variable that affects your workers’ compensation costs: your experience modification factor, often referred to as an ex-mod.

Stated simply, an ex-mod is a multiplier that relates to your claims experience. By multiplying the base rate for the applicable occupational class times your ex-mod, an insurer can reward or penalize you for your claims experience.

In most states, your premiums must exceed a certain minimum amount for the ex-mod to apply. If you do not pay enough in premiums, your organization will have a “minimum premium policy,” in which ex-mods do not apply.

Insurance companies send information on employers’ premiums and losses to the state’s rating bureau. The rating bureau then calculates ex-mods based on the employer’s paid claims and incurred losses for the “experience period,” generally the three years prior to the last policy renewal date.

To calculate your ex-mod, expressed as a percentage, take your total actual losses for this period and divide by the total expected losses, or average losses by $100 of payroll per job classification. An employer with actual losses of $253,563 and expected losses of $352,051 would calculate the experience modification as follows:

253,563

352,051 = 72%

However, it’s not as simple as all that. Not all losses are weighted equally. And rating bureaus use “weighting values” and “ballast values” to arrive at ex-mods that more accurately predict your company’s losses.

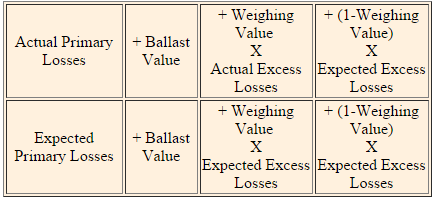

Following is the actual formula for calculating an experience modification factor:

What do these terms mean?

- “Primary losses” are the first $5,000 of any loss; “excess losses” are all loss amounts over $5,000. Losses up to $5,000 are included in full. Losses in excess of $5,000 are included on a discounted basis. In practical terms, this means that smaller losses have a bigger relative impact on your ex-mod than larger ones do.

- The “ballast value” and “weighting value” attempt to correct for the size of the risk. In statistics, the larger the pool sampled, the more accurate the sample is. Calculating ex-mods works in the same way — the larger the payroll base, the more accurately you will be able to predict your losses.

The resulting experience modification factor is expressed in a number that generally ranges from .75 to 1.75. An experience modification of 1.00 indicates your losses reached the expected dollar amount. A number higher than 1.00 indicates that your risk of loss is greater than average, while an ex-mod of less than 1.00 indicates your risk is better than average. If you meet the minimum premium levels, you can control your workers’ compensation costs by keeping your ex-mod low.

Keeping Ex-Mods Low

Keeping ex-mods low requires controlling workers’ compensation claims. Focus on controlling the smaller, more frequent losses —they will impact your ex-mods more than less frequent, larger losses.

Next, you’ll want to periodically review your payroll and claims information for accuracy. Make sure your payroll data is accurate and your ex-mod calculations include data from the proper years. And keep tabs on loss reserves — unused loss reserves affect your experience modification.

Leave a Reply